Labor market on the mend, lower rates on the fence?

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

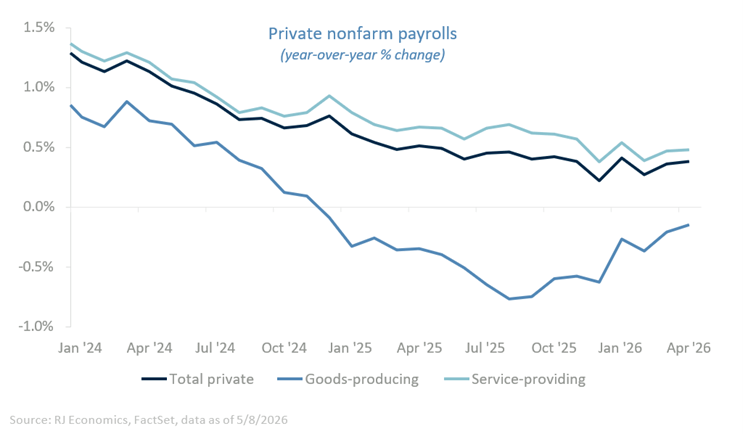

Firms pulled back sharply on hiring last year as policy uncertainty and higher input costs – driven largely by tariffs – forced a reassessment of risk. Nonfarm payroll growth averaged just 9,700 per month in 2025, down dramatically from 121,600 in 2024. That slowdown reflected a familiar corporate response: When uncertainty rises, labor – the largest and most flexible cost – becomes the primary adjustment mechanism. Rather than expand headcount, firms chose to wait.

This dynamic was most pronounced in manufacturing; ironically, the sector tariffs were intended to protect. Manufacturing payrolls weakened even as broader private-sector employment continued to grow, highlighting the disconnect between policy intent and labor market outcomes.

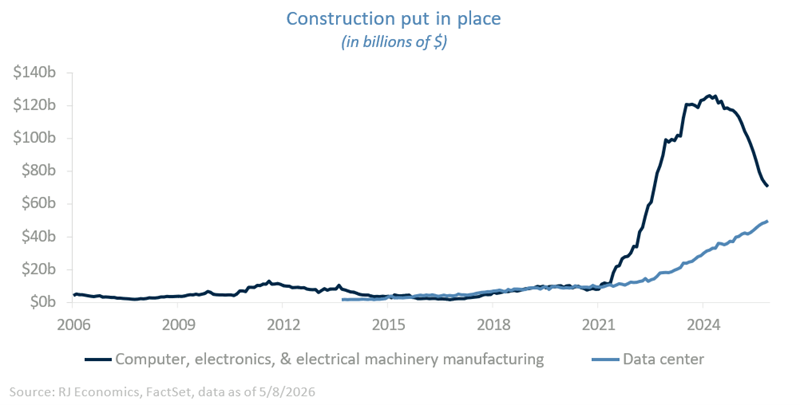

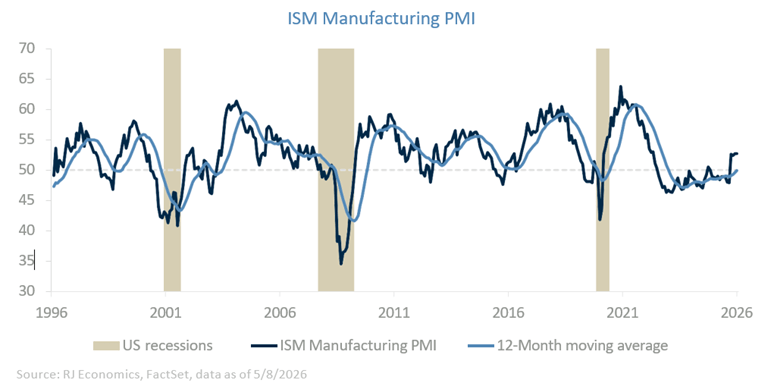

Importantly, manufacturing activity is now being driven less by trade policy and more by the lagged effects of earlier industrial policy. The investment surge sparked by the CHIPS Act and the Inflation Reduction Act pushed construction spending on manufacturing facilities to record levels beginning in 2021 to 2022. Those projects are now coming online. As new plants ramp up production – and as data center construction remains elevated amid the AI buildout – both investment spending and manufacturing output have improved, a trend reflected in the rebound in the ISM Manufacturing PMI in recent months.

What has not followed is a parallel recovery in manufacturing employment. Firms are meeting higher demand by boosting productivity rather than expanding payrolls. While productivity across the broader nonfarm business sector rose just 0.8% in the first quarter, manufacturing productivity jumped 3.6%. Over the current business cycle, manufacturing productivity has grown at an annualized pace of 0.5%, a clear improvement from the anemic 0.1% rate seen between 2007 and 2019. Even so, productivity growth remains well below its long-term average, underscoring both the progress made and the limits of the current cycle.

It is premature to credit AI investment directly for this productivity surge, but the implications are clear. Output is rising without commensurate gains in employment, helping explain why manufacturing payrolls remain under pressure even as activity improves. Perhaps, too, policy is reinforcing this dynamic: The accelerated depreciation provisions in the One Big Beautiful Bill Act allow firms to expense 100% of qualifying investments in year one, effectively lowering the after-tax cost of deploying AI and automation.

That incentive structure may tilt decision-making further toward capital deepening rather than labor hiring, especially when compared with the ongoing cost associated with expanding payrolls. This dynamic was also evident in the most recent employment report, where the information and financial activities sectors saw the largest job losses in March and have been experiencing persistent weakness for some time.

The broader labor market, however, remains resilient. April delivered another solid month of job gains, with job losses confined to a handful of sectors, including manufacturing, financial activities and information technology. Average job growth through the first four months of the year is running near 75,000 per month, broadly consistent with our expectations. Given persistent and often sizable revisions, it is still too early to revise our outlook materially.

From a policy perspective, the risk is asymmetrical. Any meaningful acceleration in hiring from here would complicate the Federal Reserve’s (Fed) ability to cut rates later this year, particularly as inflation pressures re-emerge alongside higher oil and gasoline prices. For markets, the key tension is between productivity-driven growth that supports earnings and labor market strength that keeps the Fed on hold. How that balance evolves will be critical for rate expectations in the months ahead.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.