Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Led by AI and its derivatives, 2Q25 EPS came in better than expected

- Consumer spending is a mixed bag and is poised to cool in the second half

- With S&P 500 multiples near historical highs, earnings will need to be the driver

Winding Down The Summer! While summer ‘officially’ lasts until late September, Labor Day marks its ‘unofficial’ close – and it’s fast approaching. That makes now the perfect time to hit the beach, prep and get organized for the school year, or sneak in a last-minute getaway. Speaking of winding down, guess what is wrapping up in the financial markets? 2Q25 earnings season. And with over 90% of S&P 500 companies having reported, the results have been stronger than expected. The index is on track for its third consecutive quarter of double-digit growth, up more than 11% YoY. Roughly 81% of companies beat earnings estimates – the highest rate since late 2021. Still, despite upbeat commentary from corporate leaders, the market wasn’t forgiving on earnings misses, signaling that investor sentiment remains cautious amid elevated valuations. Here are our five key takeaways from this earnings season:

- Key words on earnings calls paint a ‘sunny’ picture | Alongside strong earnings results, company call transcripts told a similarly upbeat story. Despite muted CEO confidence readings (e.g. the Conference Board) and ongoing tariff concerns, management teams struck a more optimistic tone – emphasizing resilience in the face of headwinds. Notably, ‘recession’ mentions by S&P 500 CEOs dropped to their lowest level since 2007, a sharp contrast to three months ago. While tariffs are nudging prices higher, ‘inflation’ mentions fell by ~50% compared to last quarter. Finally, corporate confidence is showing up in corporate activity: buybacks may dip slightly this quarter, but they’ve averaged $200 billion for seven straight quarters and are on track to top $1 trillion in 2025 – for the first time ever.

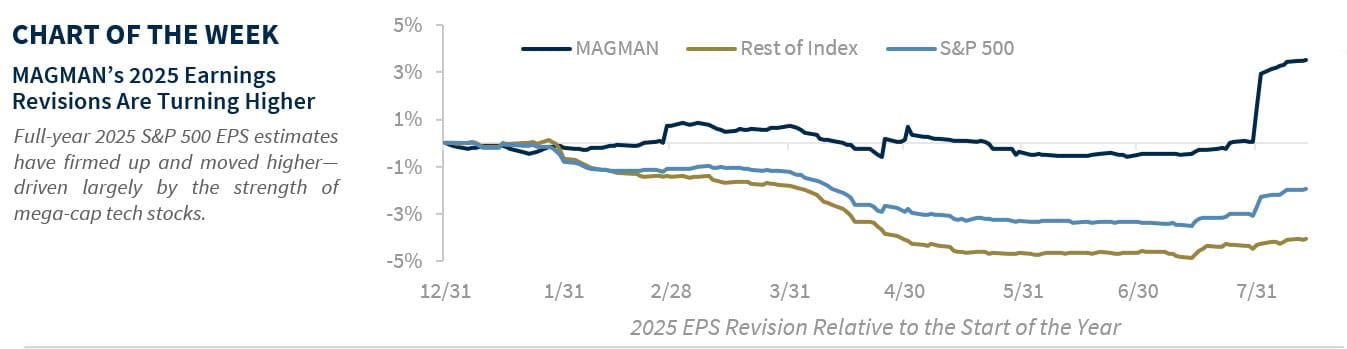

- Mega-cap tech remains the ‘bright’ spot | Since the April lows, mega-cap tech (MAGMAN*) has surged – up 50% versus 21% for the rest of the S&P 500. This earnings season backed those gains, with MAGMAN* on track for 27% YoY earnings growth – its 10th straight quarter outpacing the rest of the S&P 500 (+7%). In fact, mega-cap tech names beat their estimates by an aggregate of 13.5% – the best since 2Q23. A record number of ‘AI’ mentions include emerging use cases across a diverse set of industries, from the electric grid to pharma R&D. More capacity is needed to meet demand, and nearly all the mega-cap tech companies raised full-year EPS and capex guidance. With consensus estimates for MAGMAN EPS expected to outpace the rest of the S&P 500 each quarter through 2026, fundamental strength keeps us overweight mega-cap tech. The same applies to Industrials – a key player in powering data centers.

- Consumers on solid footing, but ‘cooldown’ evident under the surface | Consumer behavior remains mixed. Banks and credit card companies report healthy consumer spending overall, though lower-income consumers continue to face challenges. Still, firms focused on sub-prime borrowers – like Synchrony Financial and Capital One – have noted some improvement in credit quality. Beneath the surface, spending is uneven. Consumers are more selective, prioritizing experiences like travel (as seen in the solid TSA screening data) over goods – especially those hit by tariffs, such as home appliances. This trend shows up across industries too: full-service restaurants, offering better value propositions, outperformed fast casual. While the consumer is navigating a whirlwind of economic changes, expectations of a weaker labor market in 2H25 should lead to a moderation in spending in the months ahead. We’ll get fresh insights next week when Walmart, Target, Home Depot, and Lowe’s report results for the quarter ending July 31.

- Tariffs are ‘clouding’ the outlook | Companies have shown resilience in navigating tariffs—adjusting supply chains, negotiating with foreign suppliers, and substituting goods – helping protect margins so far. But pressure is building. For example, diversified goods companies such as Amazon, Walmart and Procter & Gamble have raised prices due to tariffs. Smaller firms have not gone unscathed. Case in point: beer companies are paying up for aluminum, and medical device firms are citing rising component costs. With the newly increased tariff rates now in effect as of August 7, the full impact of tariffs will likely be felt in 2H25. So far, earnings results have handily exceeded expectations—but this week’s hot PPI report offered a preview of input cost pressures that are still ahead.

- Forward-looking estimates have ‘heated up’ | Strong 2Q25 results and upbeat guidance have lifted S&P 500 forward EPS estimates. Full-year S&P 500 EPS is now projected at $266/share – the highest since April – and has only been revised down 1.6% YTD, less than the long-term average of 2.5%. Much of this resilience stems from mega-cap tech, which makes up ~30% of index earnings and has seen estimates rise ~4% YTD. In contrast, the rest of the S&P 500 has seen a ~4% decline. As analysts begin factoring in new tariffs, downward revisions are likely to pick up. With valuations elevated, earnings – not multiple expansion—will need to drive the next leg of market gains.

For a deeper dive into the 2Q25 earnings season – including key charts and analysis – we’ll be releasing a Q&A next week featuring ten critical insights. This will follow the ‘unofficial’ end of earnings season, which typically wraps up with major retailers like Walmart reporting (Aug 21).

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.