Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

Goodbye summer, hello fall! As the sun sets on another season, we’re swapping beach days and backyard barbeques for crisp mornings, vibrant foliage, football weekends, and everything pumpkin spice. Just as nature shifts from one season to the next, financial markets follow their own cycles. This summer, equity markets quietly (i.e., low volatility) climbed, with the S&P 500 posting its third-best summer performance—from Memorial Day to Labor Day—in nearly four decades. Resilient economic growth, strong corporate earnings, and rising expectations for Federal Reserve rate cuts drove that momentum. Now, as we step into fall, the economic backdrop may grow more complex. Investors are asking whether recent gains can hold, if performance is expanding beyond a narrow group of tech leaders, and whether international equities might outperform the US. Below, we recap the 3rd quarter and share what we expect to see unfold in the months ahead.

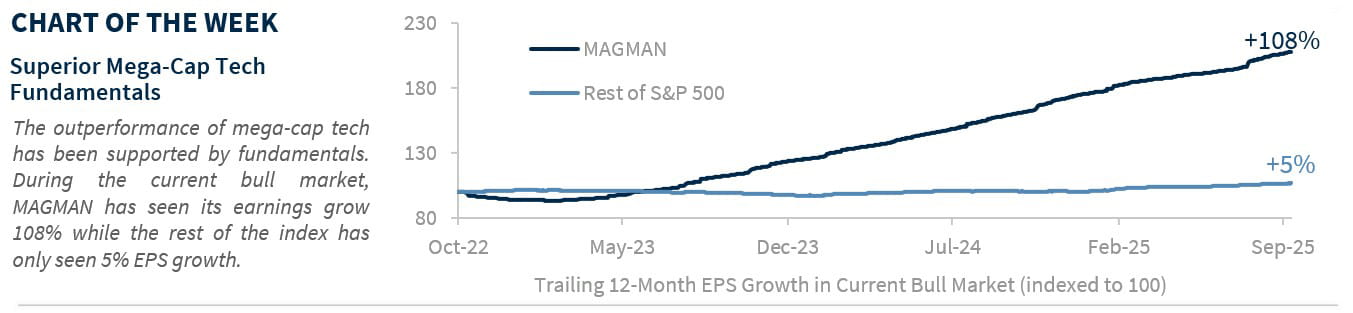

Our View: From a fundamental standpoint, MAGMAN’s 180% outperformance since the bull market began in October 2022 makes sense—its earnings have surged 108%, while the rest of the index has managed just 5% EPS growth. Looking ahead, we expect mega-cap tech to stay in front, with earnings projected to outpace both the S&P 500 and the rest of the index through 2026, thanks to sustained AI momentum. However, with the Fed resuming rate cuts and tailwinds from the new tax law poised to boost GDP growth in 2026, we see room for earnings acceleration across the rest of the index. With S&P 500 ex-MAGMAN’s EPS growth forecasted to rise from 7% in 2025 to 13% in 2026—and valuations looking more attractive—we anticipate broader participation in market gains in the months ahead.

Our View: We're cautious and maintain a neutral stance on small caps. Historically, small caps have tended to outperform after Fed cuts—especially in non-recessionary environments—and accelerating growth plus support from the new tax law could be tailwinds. Still, we favor large caps for now. Small caps face headwinds from intensifying tariff impacts, which could hit their earnings harder due to less flexible supply chains. While small caps had some brief rallies before, downward earnings revisions have often cut them short. In fact, small-cap earnings have been revised down 10% annually for three straight years. Add in less favorable sector exposure (limited tech exposure) and the fact that lower rates may already be priced in—we expect a modest increase in the 10-year Treasury yield (12-month target: 4.25%-4.50%) over the next year—and upside could be limited. We’d like to see earnings stabilize and start trending higher before turning more optimistic.

Our View: While Europe started the year strong, there are signs of flagging confidence among consumers and businesses. More broadly, we continue to favor US equities over other developed markets such as Europe and Japan. Stronger economic growth, better earnings prospects, lower tax rates, less regulation, and more favorable sector exposure—especially to Tech—support our long-term preference for US equities. We remain constructive on emerging markets (particularly Asia), where valuations remain attractive, but selectivity is key.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.