Inflation data, early earnings and geopolitics shape the market outlook

Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways:

- Warsh signals that restoring price stability is the Fed’s number one priority

- Downside inflation surprises were welcomed news for the Fed

- Early earnings results have exceeded expectations, justifying investor optimism

Financial markets were eventful this week, with key inflation reports, Federal Reserve (Fed) Chair Warsh’s first semiannual testimony to Congress, renewed Middle East tensions, and the start of earnings season all helping shape the narrative.

Despite the steady flow of headlines, the underlying message remained familiar: Inflation is still running above the Fed’s target, consumers continue to show resilience, and corporate earnings remain supportive of the equity bull market – even as geopolitical risks stay elevated. Below, we highlight five key takeaways from the week and what they may mean for the economy and financial markets.

Warsh signals inflation is his number one priority

In his inaugural semiannual testimony to Congress as Fed chair, Warsh made clear that restoring price stability remains the Fed’s top priority, emphasizing the need to rebuild credibility after inflation has run above the Federal Open Market Committee’s 2.0% target for more than five years.

While offering few clues about the policy path ahead, he reiterated that the Fed has the tools it needs – both interest rates and the balance sheet – to fulfill its mandate. More notably, Warsh renewed his call for broad reform, arguing that the Fed should reassess its communications, balance sheet strategy, data inputs, AI and labor market dynamics, and inflation framework – changes that could amount to the most significant overhaul of the Fed’s operating framework in decades. Meanwhile, this week’s softer-than-expected inflation reports should give policymakers more time to assess incoming data, keeping the Fed in a holding pattern for now.

Downside inflation surprises are good news, if sustained

This week’s downside surprises in both the Consumer Price Index (CPI) and Producer Price Index (PPI) were welcome news for the Fed. While Warsh stopped short of declaring “mission accomplished” during his Congressional testimony, noting that one month does not make a trend, June’s CPI report pointed to broad-based easing in price pressures.

Energy prices fell sharply, marking the largest monthly decline in six years and providing a meaningful drag on headline inflation. Core goods prices slipped 0.1% as tariff-related pressures continued to fade, shelter posted its smallest increase (+0.1%) since January 2021 and services inflation cooled further. Notably, the share of CPI components rising at an annualized rate above 2% fell to its lowest level since 2021. If these trends persist, inflation has likely peaked. However, renewed geopolitical tensions could still pose an upside risk to inflation and the Fed’s policy outlook.

The Iran conflict is still not behind us

After the US-Iran interim peace deal unraveled last week, hostilities quickly intensified. Airstrikes resumed, the US reinstated its blockade of Iranian ports and shipping through the Strait of Hormuz dropped by more than half, with the seven-day average falling from roughly 25 crossings to just nine. The renewed disruption lifted oil prices, with WTI climbing ~16% from its recent low to around $80 per barrel – a reminder that this conflict remains a risk, even as financial markets have largely shrugged off the latest escalation.

One underappreciated risk bears watching: The Strategic Petroleum Reserve sits near its lowest level in more than four decades, while commercial inventories have also been declining, leaving energy markets more exposed the longer this latest escalation persists. Even so, our base case does not call for a sustained rise in oil prices, as neither side has much incentive to prolong the conflict.

Consumer spending remains a growth tailwind

Despite higher gas prices and lingering inflation pressures, this week’s data reinforced the resilience of the US consumer. Real-time indicators, including restaurant bookings and department store spending, remained firmly positive year over year. Fueled in part by World Cup-related travel, hotel occupancy rose on a year-over-year basis for the 12th straight week.

That strength was also echoed in bank earnings, where major lenders pointed to broad-based consumer strength: Credit card spending grew at its fastest pace in three years, while charge-offs and delinquency rates continued to improve. With consumer spending accounting for ~70% of GDP, solid household demand should continue to support economic growth.

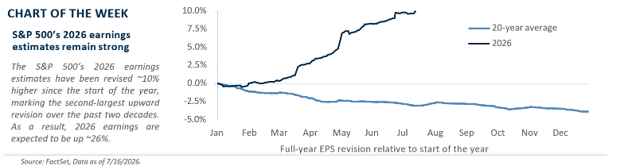

Earnings continue to clear a high bar

The bar was high heading into earnings season, with 2Q26 earnings-per-share (EPS) estimates rising ~3% in the 12 weeks before reporting began. Full-year 2026 EPS estimates are also up ~10% YTD, marking the second-largest upward revision of the past two decades.

While still early, corporate results have largely justified that optimism. Companies representing ~13% of the S&P 500’s market cap have reported thus far, with 85% beating earnings estimates and delivering aggregate profits 15% above expectations. The strength has been broad-based, from record bank earnings fueled by robust investment banking and IPO activity to strong sales growth at select industrial firms and upside surprises from key health insurers. With valuations already elevated, earnings will need to carry the market from here, and early results suggest they are up to the task.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.