Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Economic headwinds from trade policies are still ahead

- Tax cuts not likely to fully offset the impact from tariffs

- Treasury yields are moving into the danger zone for equities

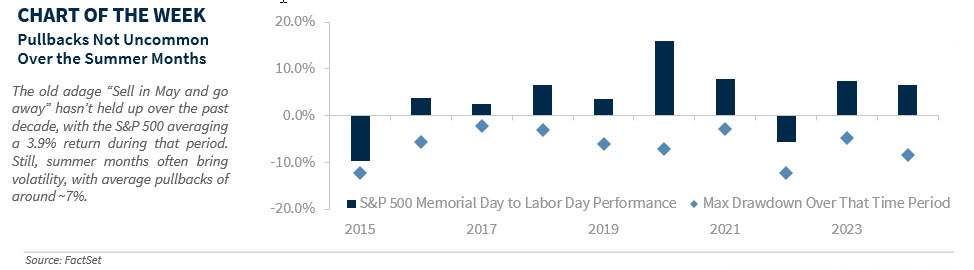

Sell in May and Go Away? This old market saying tends to resurface around Memorial Day, suggesting investors should scale back their equity exposure ahead of what’s perceived as a seasonally weaker stretch for stocks. While the phrase is catchy and rhymes well, its track record is less than reliable. History shows the S&P 500 tends to deliver solid returns between Memorial Day and Labor Day. Over the past decade, the index has averaged a 3.9% gain (~15% annualized) during this period and finished positive 80% of the time. That said, summer isn’t without risk. The S&P 500 has historically seen an average drawdown of ~7% at some point during these months, often sparked by major global events, like the euro debt crisis, China-related volatility, or the US credit downgrade. With that in mind, here are three reasons we’re cautious heading into summer:

- Delayed Tariff Impacts On The Economy Are Still Ahead | Despite the soft ‘headline’ GDP print for 1Q25 (-0.3%), underlying economic momentum has remained resilient. However, our economist expects growth to slow through the rest of the year (RJ 2025 GDP forecast: ~1%) as the effects of President Trump’s trade policies increasingly weigh on consumer spending and business investment.

- Tariffs—Financial markets welcomed the temporary trade truce between the US and China, but it’s too soon to declare victory. While the news is encouraging, trade tensions remain far from resolved—evident by the tariff threats on the EU this morning. Aside from a preliminary deal with the UK, progress on other fronts has been limited—leaving much to be done before the 90-day reprieves expire. Currently, the US is halfway through the 90-day pause on ‘reciprocal’ tariffs for all countries except China, which ends on July 8. Negotiations with China have a bit more runway, with their pause set to expire on August 12. Uncertainty also lingers around the next potential flashpoint, especially as President Trump has signaled plans to move forward with sector-specific tariffs targeting areas like pharmaceuticals and semiconductors. While markets cheered the recent de-escalation and the rollback of some punitive tariffs on China, the economic impact of a 15–17% average effective tariff rate—5x higher than at the start of the year—has yet to be fully felt. This sharp increase is likely to weigh on economic activity and contribute to further softening in the labor market in the months ahead.

- Earnings— S&P 500 earnings got off to a strong start in Q1 2025, rising +14% year-over-year—double the consensus expectations at the beginning of the quarter. However, since most companies reported results for the period prior to President Trump’s tariff announcements on Liberation Day (April 2), the numbers don’t fully reflect the economic impact of the new trade landscape. While the S&P 500 bounced back on news of a trade truce, expectations for a tougher economic backdrop—marked by slowing sales growth and rising input costs—have caused earnings estimates to trend lower. Full-year 2025 EPS estimates have declined from $272 at the start of the year to $263, still implying 10% YoY growth. However, we believe the consensus remains too optimistic given the mounting economic headwinds and uncertainty around the level and duration of the tariffs. We remain comfortable with our below-consensus EPS forecast of $250–$255 and expect further downward revisions to weigh on equity markets in the near term.

- Tax Cuts Not Likely To Fully Offset Tariff Impacts | Investors may hope President Trump’s proposed tax and spending bill will offset the drag from tariffs, especially with the passage of the tax bill expected as early as July. But our analysis suggests that’s unlikely in the near term. About 86% of the bill’s cost comes from extending the 2017 tax cuts, offering little new stimulus. While there are fresh proposals—like eliminating taxes on tips and expanding SALT deductions—they’re partially offset by spending cuts. Meanwhile, tariffs are already weighing on growth, and any tax benefits likely won’t be felt until 2026. The result: a policy mix that could hamper growth in the near term.

- Yields Moving Into The Danger Zone For Equities | The 10-year Treasury yield has continued its upward climb, reaching a three-month high. Notably, the last time yields pushed above 4.5%—and continued rising—it was driven by optimism around stronger economic growth, a good thing for earnings growth. That’s not the case this time. Instead, the rise is being fueled by growing concerns over persistent budget deficits—a far less reassuring backdrop. With the 10-year yield now above the key 4.50% threshold, we believe caution is warranted for two reasons. First, this level has historically challenged investor sentiment. It also coincides with another critical rate: a 7% 30-year mortgage, which could further strain housing demand and broader economic activity. Second, equity valuations tend to move inversely with interest rates. When yields hit 4.5%, the S&P 500’s price-to-earnings (P/E) ratio has historically struggled to expand—and has even contracted. A move toward 4.75% would be even more concerning, as equities have typically underperformed at that level. Taken together—with rising yields and the likelihood of further downward in consensus EPS estimates—we believe our more cautious stance on equities is justified.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.