Let the games begin: markets vs. the Fed

- 03.20.26

- Economy & Policy

- Commentary

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

Several days after the end of the Federal Open Market Committee (FOMC) meeting, markets are starting to second guess the Federal Reserve (Fed) in what is going to be an interesting battle of wills.

Sometimes markets try to outmaneuver the Fed’s decisions, pushing the Fed to agree with their view, while other times the Fed tries to push back if markets are, according to the Fed, way out of line with their thinking regarding interest rates. In the end the relationship is more symbiotic, as the Fed doesn’t like to go against the markets. However, in several situations in the past, when the Fed thinks there are problems brewing ahead, it has no problem surprising markets, be it by pulling an emergency interest rate cut or an interest rate increase.

We don’t think we are close to a surprise move from the Fed any time soon, but the Fed chair’s commentary regarding current uncertainty is probably a harbinger for things to come, and we need to start talking about it. The biggest problem is that even the direction of a potential surprise is, let’s say, uncertain. That is, is the focus employment or inflation? If it is employment and thus a potential recession, then we could get lower interest rates because under those conditions, inflation should not be a sustained issue. However, if core inflation starts to move higher, the Fed will have to weigh the risks of not acting and be accused again of being late and allowing higher headline prices to permeate into core inflation. This time around, the inflation leash is very short.

Before the runup in inflation in 2021, the Fed had said that it was going to wait and could accept inflation running slightly above the 2% target for some time, which in hindsight was a big mistake. Although this strategy was the conclusion reached during the pre-pandemic period, when the Fed had difficulty bringing inflation up to the 2% target from below, today’s environment does not give the Fed such flexibility. Today, as soon as the Fed has any indication that core prices are starting to go up, it has to start increasing rates. As we said above, the only thing that will prevent this is if the Fed is concerned about an ensuing recession.

Two weeks ago, markets had priced in two rate cuts this year while the Fed had penciled in just one cut. Today, markets have turned the tables and are now pricing in no rate cuts during this year, while the Fed has left its rate cuts at one after Wednesday’s FOMC decision. However, there was very little conviction from the Fed chair on Wednesday that it actually knew what it was going to do this year. That is, if it is, normally, data dependent, the uncertainty about the current environment, with tariff policy changes still lingering and now this petroleum and gasoline price shock, there is less conviction/certainty regarding the path forward today.

Geopolitical risks distort price signals

The administration has been looking for ways to bring down gasoline prices, but most of the ideas being discussed are unlikely to make a meaningful difference. Temporarily suspending the Jones Act, for example, is not expected to lower gasoline prices, according to Raymond James strategist Pavel Molchanov. Meetings with oil companies and even talk of restricting oil exports are also unlikely to help. In fact, some of these measures could backfire and push prices higher rather than lower.

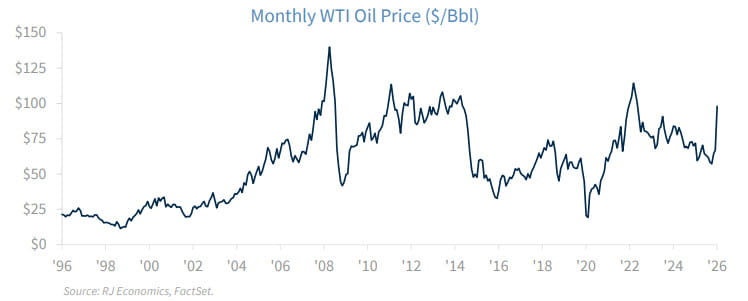

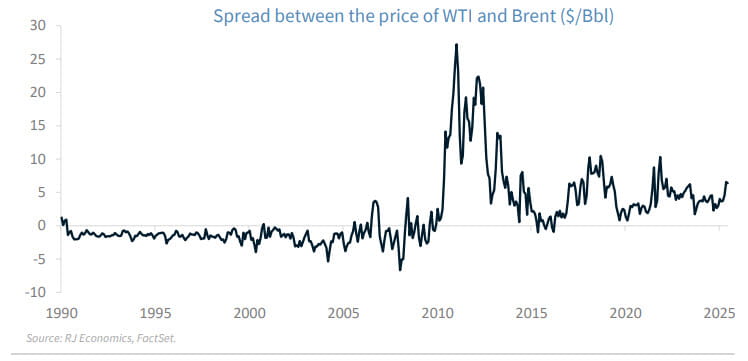

Gasoline prices are shaped by global market forces, not short‑term policy actions. What really matters is what happens during geopolitical crises that disrupt oil supplies. In those moments, the usual relationship between oil prices and gasoline prices breaks down. Historically, US gasoline prices move closely with oil prices, whether measured by the US benchmark (WTI) or the global benchmark (Brent). But during periods of global stress – such as the early 2010s – that relationship weakened sharply. At that time, the price gap between US and global oil surged, and gasoline prices followed global oil prices much more closely than US benchmarks. A similar pattern appears to be emerging today.

This helps explain why gasoline prices can rise even when US oil production is strong. Although the US now produces more oil than it consumes, it still exports lighter crude and imports heavier crude that US refineries need. As a result, global supply disruptions continue to play an outsized role in determining what US consumers pay at the pump. In short, during geopolitical crises, international oil markets matter more for gasoline prices than domestic production alone.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.