Geopolitical disturbance, market volatility, and bond opportunities

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

The world has been facing geopolitical disturbances for years, with Russia’s invasion of Ukraine and Israel’s conflict with Hezbollah. The United States and Israel entanglement with Iran has slowed oil transport, cutting off shipping through the Strait of Hormuz. Investors must now evaluate whether this is temporary or a skirmish destined to extend for months, if not years. The consequences of these conflicts send shockwaves through financial markets; while looming actions could trigger catastrophic market events.

The short-term effects have pushed oil prices from $67 to $97 per barrel in just three weeks. Soaring oil prices threaten to fuel inflation, which in turn puts more pressure on the Federal Reserve. The Fed was believed to be poised to cut rates a few times in 2026, easing economic conditions amid a weakening labor market. However, with the current inflation backdrop, all considerations must be reevaluated. Other central banks, such as the European Central Bank and the Bank of England, are discussing raising interest rates, considering geopolitical disruptions.

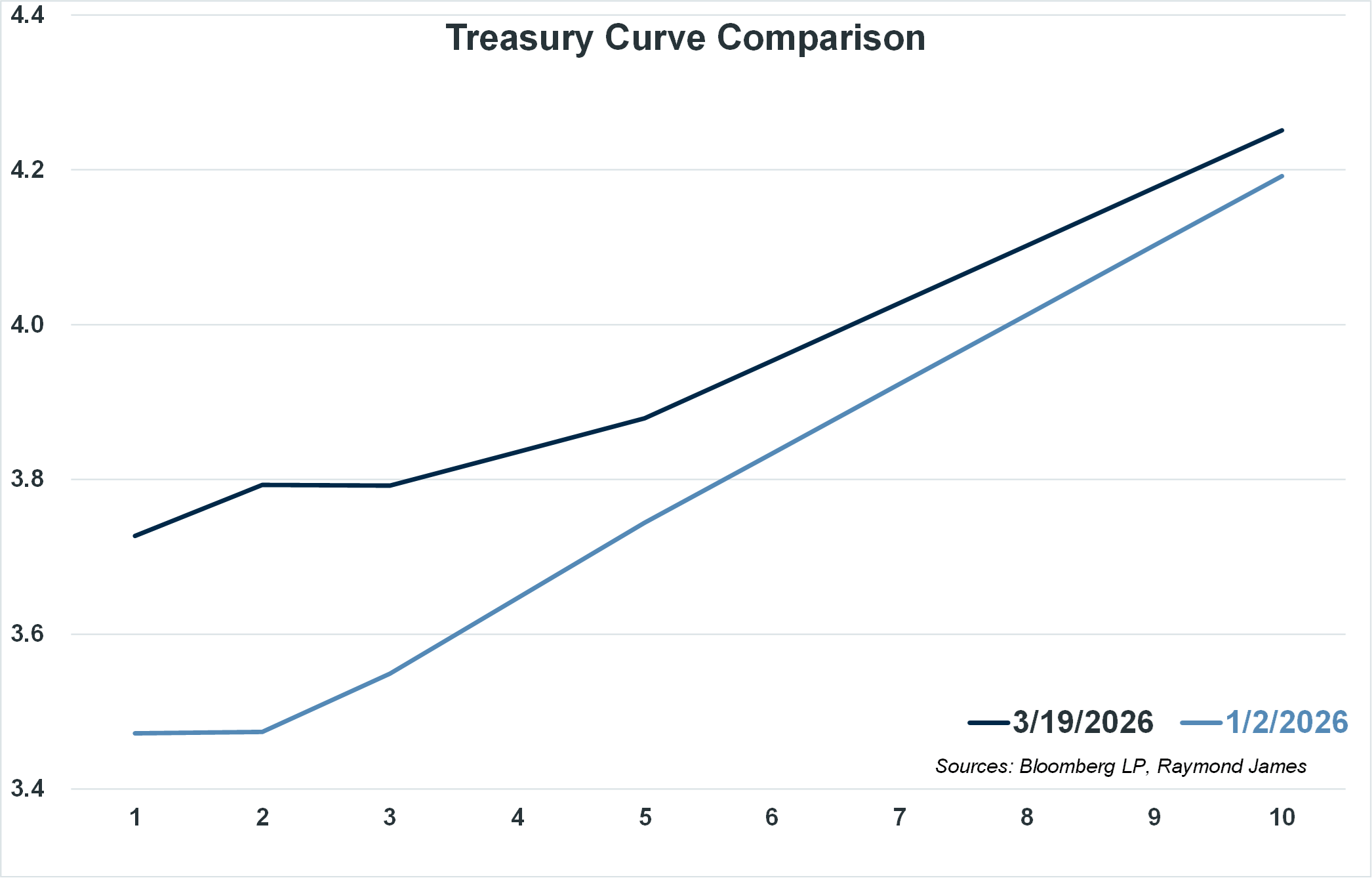

The stock market has now experienced four consecutive “down” weeks. Conversely, increasing oil prices have pulled short-term Treasury prices lower, or in other words, pushed short-term yields up. For weeks, we’ve discussed the emotional side of investing. The consequential impact on financial markets can be directly tied to recent geopolitical activity. The graph on the right shows the jump in short-term interest rates year to date. The hardest part to evaluate can be the news, not the math associated with portfolio holdings. What do I mean?

The inverse relationship between a bond’s price and yield indicates that bonds purchased just a few weeks ago will reflect a “red,” or lower, portfolio value since market prices have dropped. What the headlines don’t reveal is one of the protective features of individual bonds. That is, when a bond is purchased and held to maturity, interim price fluctuations have no effect on the bond’s cash flow, income stream, or the time when all invested money will be returned to the investor. This reality is distinct from that of a stock, which often depends on price appreciation to generate value over a holding period.

Furthermore, the higher-yield environment creates an opportunity to boost portfolio income while shifting toward lower-risk assets. The opportunity to buy yield is being extended by current events. It is important to keep all of this in perspective. Just four years ago, investors did not have the income opportunities that exist today. Although geopolitical events have created volatility, the resulting fixed-income opportunities can positively impact long-term portfolio outcomes.

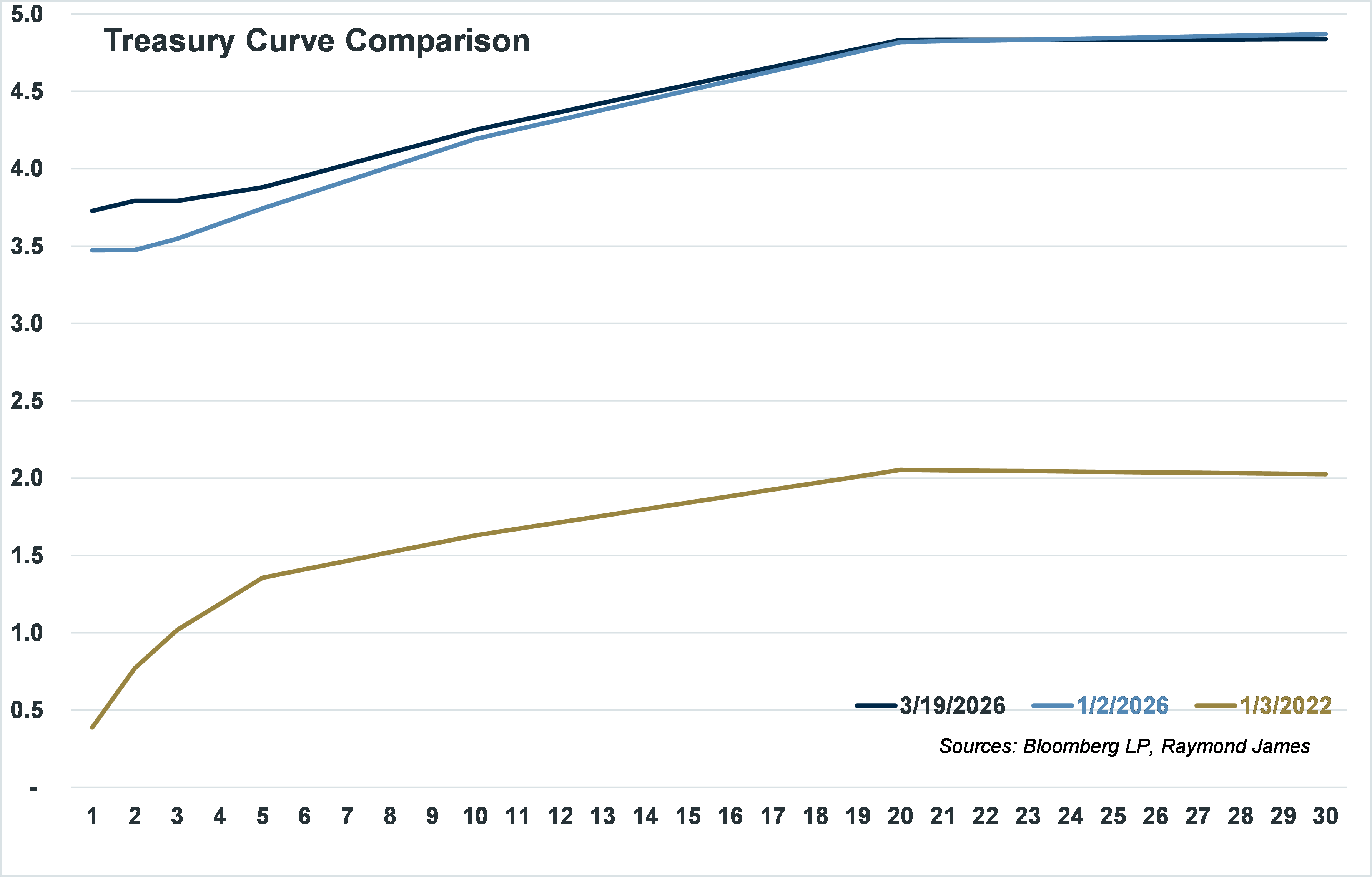

Putting the short-term jump in interest rates into perspective, the following graph shows that income opportunities exist across the entire yield curve when viewed relative to historic rates. It is easy to get caught up in the moment, but the contributions to the fixed income allocation are long-term. Don’t discount longstanding strategies due to momentary geopolitical disturbances. Individual bonds offer three distinct benefits: reduce market risk, capture cash flow streams, and, at current levels, lock in longer-term, high levels of income.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.